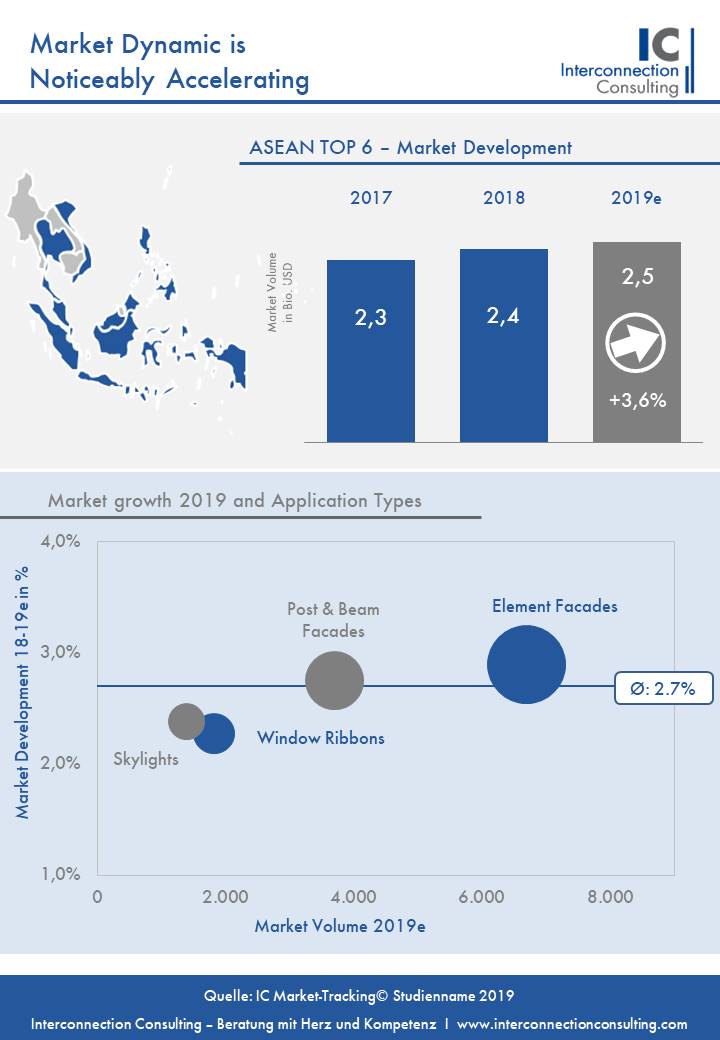

As one of the leading market research institutes in the world in the area of façades, Interconnection Consulting regularly examines almost the entire spectrum of the facade market.

This includes sandwich panels with a wide range of different materials (steel, aluminum, and others) and various core materials (PUR/PIR, mineral wool, etc.), curtain wall facades (also known as elemental facades, mullion and transom facades, or unitized curtain walls,…

> read more

Facades

Market Report, Industry Report, Market Study, Industry Analysis

Detailed Market Data and Information about Sandwich Panels

Facades

Katarina Hornikova

> Learn more about Katarina Hornikova

Katarina Hornikova has been working for Interconnection Consulting since 2017. She specializes in international business strategies, international marketing, as well as the development tendencies of the specific international goods markets. She is responsible for the preparation of studies and market forecasting models within the construction industry. She studied International Trade Management and International Business.

Contact me without obligation, I support you gladly!

Report Offers

These industries might be interesting for you too

IC News

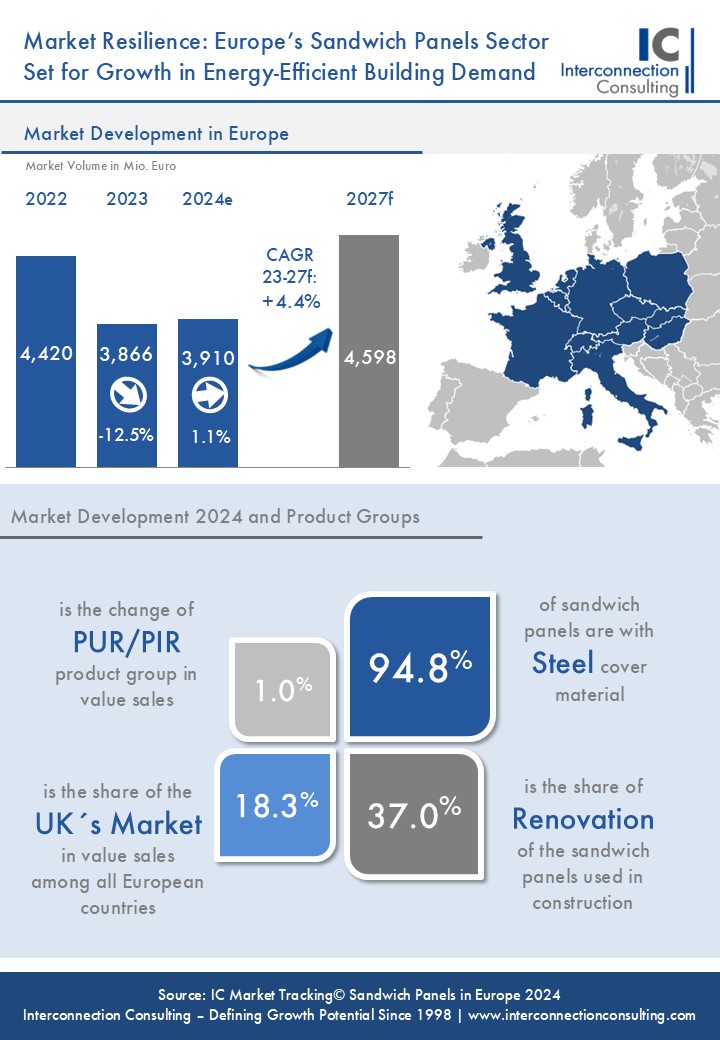

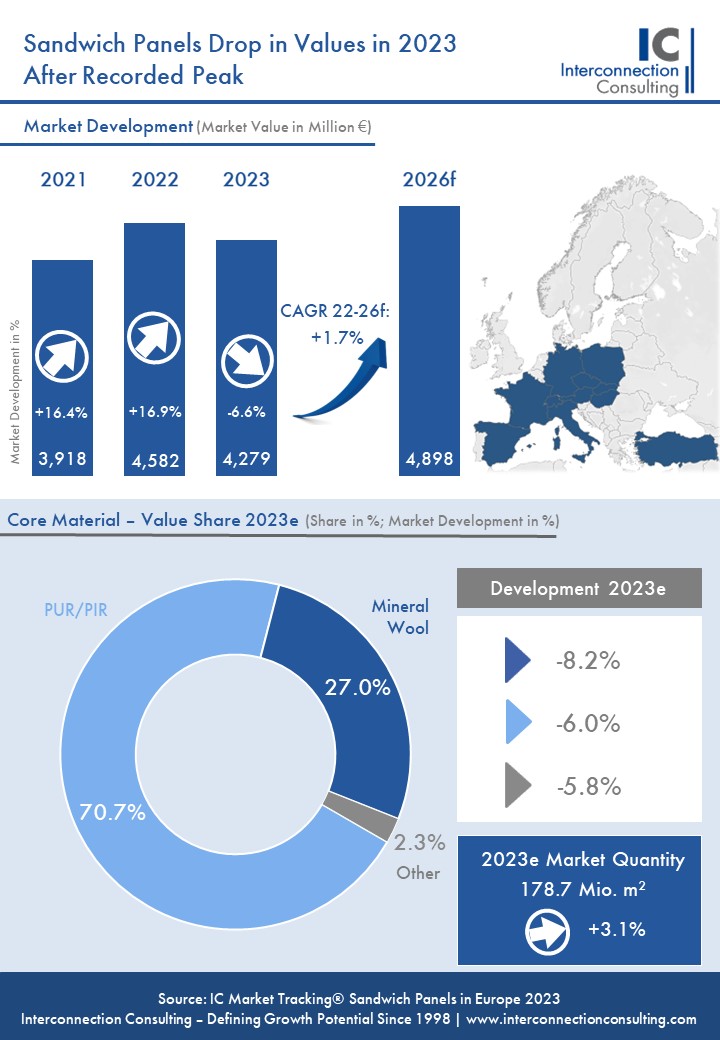

From Record Highs to a Downturn: European Sandwich Panels Market Faces a 7% Value Drop in 2023 After a Historic Year in 2022

Leading Companies trust in Interconnection Consulting

Kontron

The most important benefit of the Impulsworkshop "sales optimization" was in my view the procedure of the definition of strengths and the entire sales process. Mr. Berger is very competent and professional. Fabian Freund (Sales Manager, Kontron Austria)

ELK

The prefabricated housing study by Interconnection Consulting shows a real picture of the actual market situation and forms a valuable basis for our strategic decisions.

Gerhard Schuller (CFO ELK)

ELK

The prefabricated housing study by Interconnection Consulting shows a real picture of the actual market situation and forms a valuable basis for our strategic decisions.

Gerhard Schuller (CFO ELK)

Epson

EPSON is satisfied with the Interconnection's way of communication with the market and with clients. EPSON is also appriciate the Interconnection's continuous work trying to aim the report to be at the higher level. As a result, EPSON rely on Interconnection data, for the market of POS Printers and Systems.

T.Murakami (Brand Management, Seiko Epson Corporation)

Gaulhofer

I appreciate on the forum "Impulsworkshop Vertriebsoptimierung" the practical relevance of Peter Berger linked with his practical examples. I also liked the sovereign presentation style. The most important benefit was for me, on the one hand refresh of methods and also the sales management tools that were shown. Ing. Dietmar Hammer (Head of Product Management Gaulhofer)

Kontron

The most important benefit of the Impulsworkshop "sales optimization" was in my view the procedure of the definition of strengths and the entire sales process. Mr. Berger is very competent and professional. Fabian Freund (Sales Manager, Kontron Austria)

Österreichs Personaldienstleister

The sales management tool "Jobs Intelligence Austria" has become indispensable for many Austrian temporary staffing providers for fast and correct strategic management decisions as well as a daily support tool for hot leads for the sales team. Interconnection Consulting has consider individually to all user needs during development process and also convinces with fast response times during operation.

Dr. Gertraud Höltl (Generalsekretärin Österreichs Personal Dienstleister)

Saint Gobain

Long experience and deep understanding of the construciton industry markets make up the quality of the IC studies. Interconnection Consulting is a constant companion concerning the assessment of markets and helpful for decision-making.

Bernd Blümmers (Directeur General, Saint-Gobain Solar Systems, Central Europe, Aachen)

Salamander

Interconnection Consulting reports deliver a worthfull external perspective and are so a good contrast with regards to our internal market point of views.

Pedro Posada (CEO Salamander Industrial Products Spain)

Scandinavian Business Seating

The IC Report gives a very good overview of the Western European office furniture market, in a well-structured way. The data is helpful to better understand the market developments and drivers.

Beatrice Sotelo (Director Business Development , Scandinavian Business Seating)

Schneider Electric

Under a short time constraint, Interconnection was able to deliver an outstanding study that exceeded my expectation in terms of quality and market breadth. I highly recommend Interconnection to anyone in need of market research.

Jeff Canterberry (Director of Strategy and M&A, Schneider Electric)

Sodexo

When developing new market strategies, Interconnection is a trusted source we always come back to. Christian Frey (Marketing Manager CS DACH)

Do not hesitate to contact us

Please describe your needs or request a callback. We look forward to hearing from you and contact you immediately.